It may seem like a nearly impossible task to get a mortgage after retirement, but there are ways you can do it even if you are not employed. If you’re planning to apply for a mortgage, here are 5 common questions you might ask that we’ve answered for you:

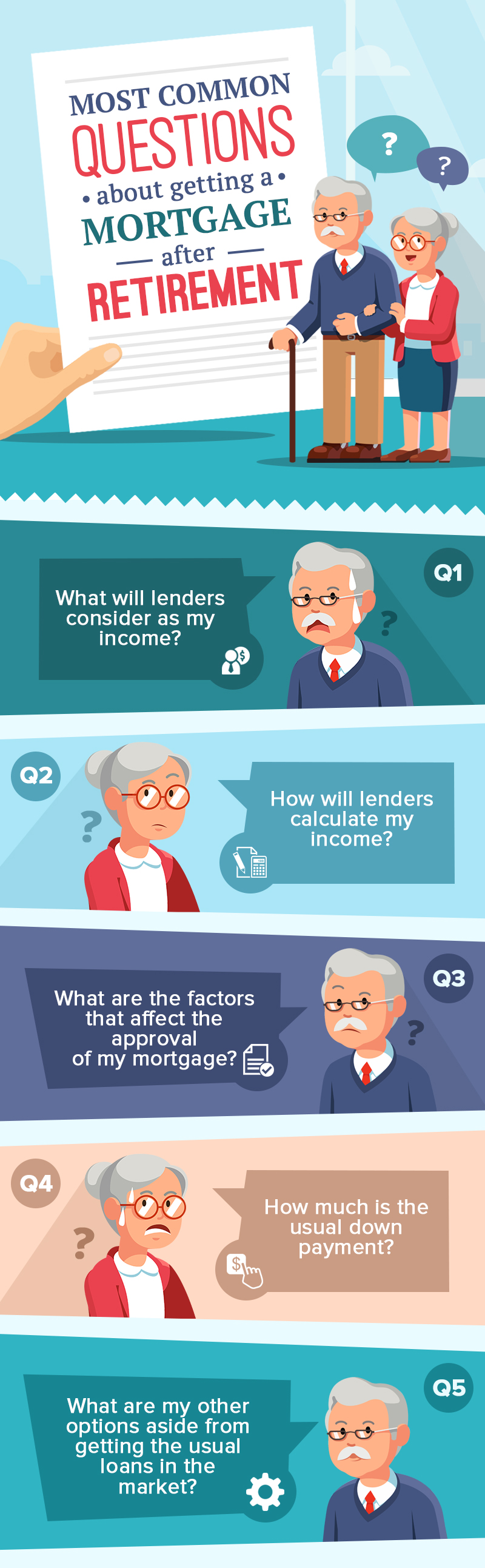

1. What will lenders consider as my income?

Income from a regular or part-time job

A brokerage account or retirement savings

Transfer payments like Social Security and your pension

Invested assets

Household income (income from non-borrowing household members)

2. How will lenders calculate my income?

If you are not employed, there are two methods that lenders will use to calculate your income. Take note that if you receive transfer payments, those will be included in the computation for your income in both of these methods.

Asset depletion method: If you have a lot of invested assets, the lender will calculate their current aggregate value and will subtract the amount for the down payment and closing costs. 70% of what remains will then be divided by 360, which is the number of months’ payment on a 30-year mortgage.

Drawdown from retirement method: If you’re at least 59 ½ years old, you can use documents or receipts that verify your recent withdrawals from retirement accounts.

3. What are the factors that can affect the approval of my mortgage application?

Aside from the above, some of your other financial details will also be subject to the lender's scrutiny.

Credit score: The typical requirement of lenders for a credit score is usually 780; a score that's higher than that can increase your chances of getting approved. And if you ever fall short on other factors, such as debt to income ratio, a good credit score just might save your application. Also, if your score is higher than that, you could also get a better interest rate.

Debt to income ratio: Your debt is comprised of car payments, credit card minimum payments and your total projected house payment which includes interest, principal, property taxes and insurance. Other things like alimony and child support are also included in it. The debt to income ratio is expressed as a percentage, and is computed by dividing your total monthly debt by your gross monthly income. The safe percentage among lenders is generally considered to be 43% or lower, but maximum DTI still varies per lender. The ideal is 36%, and with no more than 28% going into paying the mortgage.

House expense ratio: Your housing expense ratio is the sum of your housing payments such as the potential mortgage principal and interest payments, property taxes, mortgage insurance, hazard insurance, and association fees. It’s computed by dividing the sum of those by your pre-tax income. Just like the DTI, it is expressed as a percentage and is ideally not to exceed 36% of your income.

Post-closing liquidity: Your lender would also want to see your available liquid assets after closing, and they usually require that you have assets that could cover at least 6 months’ worth of housing expenses. This is calculated by adding up all of your verified financial assets and then subtracting the closing costs and equity for the loan.

4. How much is the usual down payment?

The amount of down payment you would have to give is dependent on the method used for determining your income.

5. What are my other options aside from getting the usual loans in the market?

VA loans: If you’re a veteran or a military spouse, VA loans offer 0 down payment and low interest rates.

Reverse mortgage: Also known as the Home Equity Conversion Mortgage (HECM) for purchase program, it is a kind of loan that can delay repaying the mortgage (principal or interest) until the house is sold or until the death of the borrower.

Here are some tips for when you’re getting a mortgage after retirement:

1. Getting a mortgage for your primary residence will result in a lower interest rate,

while a mortgage on a home that will be used for vacation or investment

purposes will have higher interest rates.

2. If you can, make extra mortgage payments. If you can afford to pay more than what the lender calculated, you can arrange to have the monthly payment increased. This can shorten the time you would have to pay for the mortgage and could decrease your monthly payments over time, and decrease the amount of interest you need to pay on the

mortgage overall.

3. If you plan to take out a hefty amount of cash for the down payment from an IRA or another tax-deferred retirement plan, take note that you might also be placed in a higher tax bracket.

4. Know about the consequences to inflation hits or a great increase in your property taxes. You also have to consider having a financial contingency plan should there ever be medical emergencies, or a price increase in your health insurance. Take these into account and get an estimate if you can still cover these events on top of your mortgage.